What is a biological asset according to IAS 41 — and why does this matter for agriculture?

High-performance livestock farming is undergoing a structural transformation. The competitive advantage is no longer solely based on production scale, but rather on the genetic quality incorporated into the herds. In this context, understanding the economic nature of genetics becomes essential.

But how does international accounting view this type of asset?

The definition of a biological asset according to IAS 41

IAS 41, an international standard issued by the International Accounting Standards Board (IASB), defines a biological asset as a living animal or plant controlled by an entity and from which future economic benefits are expected.

Although the definition seems simple, its implications are profound.

For something to be considered an asset, three elements must be present: control, expectation of future economic benefit, and the possibility of reliable measurement. When these criteria are met, we are not dealing with an operational cost, but with a structuring asset.

Practical application in bovine genetics

When we apply this logic to advanced genetic livestock farming, the framework becomes clear.

An embryo produced through in vitro fertilization, with formal identification of the donor, bull, production method, and technical registration, has defined control, proven origin, and revenue-generating potential. It is not merely a productive input—it is a biological asset.

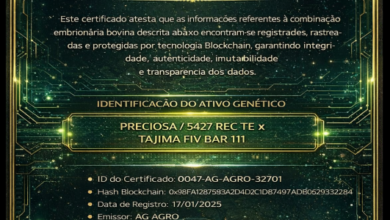

The existence of formal technical certification reinforces this condition. An example is Certificate No. 31327, issued by a company specializing in reproductive biotechnology, which records the production method, OPU date, genetic identification, and Wagyu Kuroge breed. This documentation allows for traceability, auditing, and formal inventory.

The asset ceases to be abstract. It becomes verifiable.

Why does this matter to agriculture?

The difference between treating genetics as a cost or as an asset completely alters the economic logic of the business.

When recognized as a biological asset, genetics can form part of wealth, support financial models, and integrate into more sophisticated governance structures. This shift in mindset expands the sector's ability to engage with investors, financial institutions, and structured markets.

The international movement confirms this trend. Companies like Eggschain have developed patented solutions to track genetic material using blockchain (Eggschain Secures First Patent…), creating digital chains of custody for embryos and biospecimens. In this context, technology does not replace the biological asset; it organizes its integrity and transparency.

The order is clear: first the assets, then the infrastructure.

A strategic issue

In Brazilian agriculture, it is still common for genetics to be treated exclusively as an operational expense. This view limits the potential for asset structuring.

When understood from the perspective of IAS 41, genetics takes on a different level. It becomes the basis for strategic decisions, asset organization, and sustainable expansion.

Accounting standards provide the technical language.

Biotechnology provides the materiality.

The market provides the economic validation.

When these elements align, genetics ceases to be merely a productive tool and becomes recognized as a strategic asset.

And every solid strategy begins with a correct understanding of the asset.